The global Automotive Driver Monitoring Systems market is expected to grow at the CAGR of 5.49% during the forecast period 2022-2030.

The driving monitoring system includes a camera-based driver monitoring system (DMS) pointed at the driver’s face which provides a real-time evaluation of the presence and the state of the driver. Driver Monitoring System was first introduced by Toyota in 2006 for its latest models.

DMS can help provide alerts to the driver and initiate an intervention to manage the control of the vehicle. The DMS functions co-operate with the Pre-Collision System.

DMS uses infrared sensors to monitor driver attentiveness. Specifically, the Driver Monitoring System includes a camera placed on the steering area which is capable of eye tracking via infrared detectors.

If the driver is not paying attention to the road ahead and a dangerous situation is detected, the system will warn the driver by flashing lights, warning sounds. If no action is taken, the vehicle will apply the brakes.

The driver monitoring system ensures that the driver is prepared to take control of the vehicle when the situation dictates. Beyond the driver, occupant monitoring systems can be valuable to understand their condition and even to provide a tailored environment specific to an identified occupant.

Growing consumer demand for DMS, and intense competition in the global market is compelling automotive OEMs to integrate DMS in vehicles and other higher safety features, considering the state and health of the driver which includes fatigue, and cognitive load is another major factor expected to drive growth of the global driver monitoring systems (DMS) market.

The market is divided into material type, component type, monitoring type, vehicle type and by region

With the outbreak of COVID-19, the production and sales of automotive components came to a sudden halt in most of European countries. The global passenger volume and the total infrastructure cost decreased by 60.5% and 45.4%, respectively, in 2020. Such lowered demand has severely impacted the general automotive market in Europe and affected the businesses of the automaker OEMs, such as component manufacturers, raw materials suppliers of the automotive industry, technology providers and among others.

Various measures have been announced by the European Union to support the automotive industry with European Central Bank (ECB) announcing Pandemic Emergency Purchase Program to purchase sovereign bonds and commercial papers from member states and commercial companies to infuse €750 billion and maintain liquidity in the financial system. ECB has relaxed its norms and expressed willingness to increase its size of asset purchase for as long as needed. European Investment Bank has proposed plans to mobilize €40 billion of funds and asset-backed securities purchase program to mobilize another €10 billion of support to the industries. Since the epicenter of the pandemic has shifted from China and is at its highest severity in Europe with thousands of new cases being reported daily from countries like Italy and Spain, it would be difficult for auto manufacturers to resume production in Europe soon.

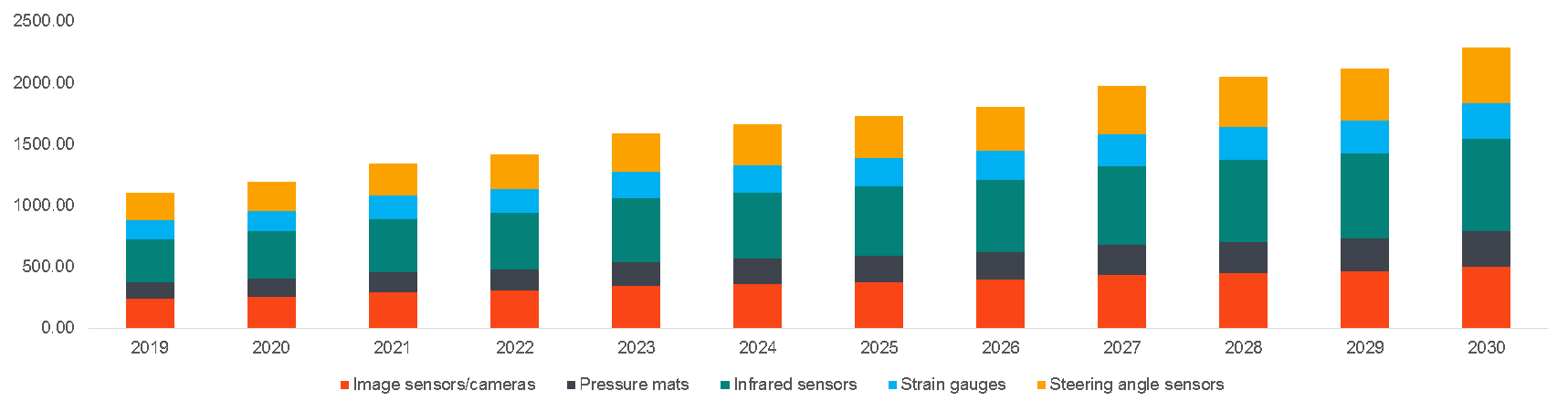

Global Automotive Driver Monitoring System includes Image sensors/cameras, Pressure mats, Infrared sensors, Strain gauges, steering angle sensor.

The infrared LED sensors detect the state of the driver and alert the driver in case of emergency, these factors make the infrared sensors segment the most dominant in the market.

Increase in road-safety awareness due to the rise in several on-road accidents caused by the driver due to fatigue and distraction is the major driver for the driver monitoring systems (DMS) market. According to publication by World Health Organization (WHO) in 2020, approximately 1.35 million people lost lives each year due to road traffic injuries.

On the basis of components, the market is bifurcated into software and hardware. The market is going to be combined with both Software and hardware segment as software and hardware systems go hand in hand. Both segments are expected to experience a rise during the forecast period.

The requirement of softwares such as GPS, are essential pertaining to tracking of vehicles and other obstacles. On the other hand devices such as camera, technologically advanced sensors plays a vital role in Automotive Driver Monitoring Systems

The driver monitoring system market consists of sales of driver monitoring systems that are used to collect recognizable information about the driver for assessing the capability of the driver to perform the driving task safely.

The market consists of revenue generated by the driver monitoring system companies manufacturing the driver manufacturing systems such as Facial Recognition/ Head Movement, heart rate monitoring, blink monitoring, steering angle sensor, and a pre-collision system.

The main types of driver monitoring systems are driver alertness/distraction monitoring, driver fatigue monitoring, drunk driving monitoring, and identity recognition.

Driver fatigue monitoring system is designed not only to accurately predict and identify situations where drowsiness and fatigue and set into a driver but also to alert those drivers so that they can pull over to the side of the road and will take other necessary steps to ensure their general safety along with the safety of other drivers.

Globally, North America is has the highest market share owing to the government support in the region, where it has played a pivotal role in driving the market for advanced driving systems by establishing safety regulations in order to reduce the traffic accidents.

Recent regulatory mandates in the in North America owing to accidents involving vehicles with partial driving automation are driving the DMS markets in these regions. However, these rapid developments, the COVID-19 pandemic, and cost concerns pose market challenges, impeding DMS penetration.

Some of the prominent companies manufacturing Automotive Driver Monitoring System products include Robert Bosch, Continental, Delphi, Denso, Omron Corporation, Valeo, Aisin Seiki, Magna, Visteon Corporation and Johnson Controls. Most of the companies are giant companies having diversified portfolio and have their presence across different parts of the world. The giant companies usually adopt merger and acquisition strategies as there was recent decline in the automotive components industry due to impact of corona virus across several businesses and stringent environmental regulations across developed countries.

To ensure high-level data integrity, accurate analysis, and impeccable forecasts

For complete satisfaction

On-demand customization of scope of the report to exactly meet your needs

Targeted market view to provide pertinent information and save time of readers

A faster and efficient way to cater to the needs with continuous iteration

Focus on Data Accuracy & Reliability

75+ Clients in Fortune 500

All your transactions are secured end-to-end, ensuring a satisfactory purchase

Ensure the best and affordable pricing

![]()