Eternity Insights has published an in-depth study on the Global Automotive Display Market, offering a strategic outlook on key product, technology, screen size, and application segments across major regions. The report delivers actionable intelligence aimed at empowering stakeholders to make data-driven decisions within a fast-evolving automotive electronics and infotainment ecosystem. The study period of this report spans from 2020 to 2034, incorporating historical data from 2020 to 2023, with 2024 as the base/assessment year and 2025–2034 as the forecast period. The report provides quantitative insights backed by qualitative analysis of market dynamics, emerging trends, competitive dynamics, and technological advancements shaping the automotive display ecosystem.

The report is designed based on a hybrid research methodology, combining extensive secondary research sourced from both paid databases (including ZoomInfo, Factiva, EMIS, S&P, Omdia, and others) and open-access resource (such as company annual reports, investor presentations, SEC filings, automotive trade publications, regulatory filings, and open-access industry whitepapers). The data collected from secondary research is validated through primary interviews with key stakeholders—including OEMs, Tier-1 & Tier-2 suppliers, technology developers, and automotive software providers—and supported by expert consultations with analysts and engineers specializing in the automotive display technologies.

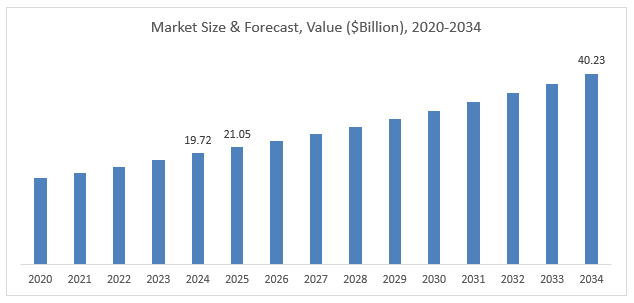

The global automotive display market is valued at $19.72 billion in 2024, projected to reach $21.05 billion in 2025, and is expected to grow at a CAGR of 7.46%, reaching approximately $40.23 billion by 2034. This growth is fueled by rising consumer expectations for in-vehicle digital experiences, the increasing integration of advanced driver assistance systems (ADAS), and the accelerating shift toward connected and electric vehicles. Automotive displays, which include instrument clusters, center stack displays, head-up displays (HUDs), rear-seat entertainment systems, and emerging augmented reality interfaces, have become central to the human-machine interface (HMI) within modern vehicles. As OEMs compete to deliver more immersive, personalized, and safer driving experiences, the demand for high-resolution, touch-enabled, and multi-screen setups continues to rise across vehicle classes.

Moreover, in countries such as the U.S., Germany, and Japan, the transition to fully digital cockpits and larger, more immersive infotainment panels is well underway, driven by premium OEMs, consumer demand for high-tech interiors, and regulatory incentives aimed at improving driver visibility, safety, and information delivery. Automakers in these markets are increasingly focusing on seamless human-machine interfaces (HMI), integrating multifunctional displays that support navigation, media, and real-time vehicle diagnostics. Meanwhile, emerging economies in Asia-Pacific and Latin America are experiencing an outstanding surge in mid-range vehicle production equipped with advanced display systems, fueled by declining component costs, localization of production, rising disposable incomes, and growing aspirations of a digitally connected middle class. As digital cockpit solutions become more affordable and scalable, their penetration across a broader range of vehicle categories is expected to accelerate globally.

Furthermore, technological advancements in OLED, mini-LED, curved displays, and augmented reality HUDs are reshaping the market landscape, enabling thinner, brighter, and more energy-efficient displays. Simultaneously, the rise of software-defined vehicles (SDVs) is amplifying the need for flexible, upgradeable display platforms that support over-the-air (OTA) updates, real-time data visualization, and seamless infotainment integration. As the automotive industry evolves toward autonomous and connected mobility, display technologies will play an increasingly vital role in delivering safe, intuitive, and engaging in-vehicle environments. The automotive display market is thus positioned for sustained expansion, driven by continuous innovation, rising vehicle digitization, and a growing emphasis on driver and passenger experience.

Rise of Vehicle Digitalization and Integrated Cockpit Modules

The automotive display market is experiencing significant growth as automakers increasingly digitize vehicle interiors to meet consumer expectations for enhanced functionality, safety, and aesthetics. The growing integration of infotainment, navigation, and instrument cluster systems into single digital cockpit modules is accelerating demand for advanced display technologies. Modern vehicles are now equipped with two or more displays, often 9 inches or larger, replacing traditional analog gauges. The trend toward combining multiple functions into a single high-resolution screen—such as CID (Central Information Display) and passenger display or cluster—has become standard, especially in mid- to high-end vehicle segments.

EU Safety Rules Fuel Demand for Larger Digital Clusters

The European Union has introduced increasingly stringent vehicle safety regulations, including mandatory integration of Advanced Driver Assistance Systems (ADAS) under the General Safety Regulation (GSR). These requirements—such as intelligent speed assistance, lane-keeping systems, driver drowsiness monitoring, and real-time hazard alerts—necessitate the use of larger, more capable digital instrument clusters to convey critical information clearly and effectively. Analog gauges and limited screen formats are no longer sufficient to support the multi-layered, dynamic data visualization needed for these systems. As a result, vehicle manufacturers are standardizing 12-inch or larger fully digital displays, particularly in compliance-focused EU markets. This regulatory environment is driving OEMs to upgrade vehicle cockpit designs across all segments, not only in premium models, further fueling demand for high-performance display technologies that can integrate ADAS visuals seamlessly with traditional driving information.

Increasing Focus Towards In-Vehicle Streaming and Gaming

As vehicles become more connected and autonomous driving features gradually reduce driver workload, consumers are increasingly viewing vehicles as extensions of their digital lifestyle. In-vehicle entertainment has evolved beyond basic audio systems, with growing interest in high-resolution rear-seat entertainment screens that support video streaming, gaming, and app-based media consumption. This trend is particularly prominent in family-oriented SUVs, luxury sedans, and ride-sharing vehicles where rear-seat comfort and experience are key selling points. With improvements in vehicle connectivity (5G, Wi-Fi), content licensing partnerships, and display quality (e.g., OLED and high-brightness LED), rear-seat displays are emerging as a competitive differentiator for OEMs.

Trade Tensions and Tariff Pressures Disrupt Supply Chains

The imposition of tariffs on Chinese-made automotive components during the Trump administration—and the continuation of many of these measures under subsequent policies—has disrupted global supply chains and increased the cost of importing display modules into the U.S. market. This has prompted several OEMs and Tier-1 suppliers to reconsider sourcing strategies, shift to alternate manufacturing hubs, or absorb higher costs, ultimately putting pressure on margins and delaying procurement cycles. While some companies have localized part of their production to mitigate the impact, the tariffs have introduced persistent uncertainty, especially for manufacturers relying heavily on Chinese panel makers.

Decline in Panel Per Vehicle Ratio and Slow Growth in Shipment Volume

While the demand for large, high-performance automotive displays is growing, the number of panels installed per vehicle is expected to decline or remain flat after 2025. Automakers are increasingly adopting integrated cockpit modules that combine multiple functions—such as cluster and infotainment—into a single large display, reducing the total number of individual screens required per vehicle. As a result, even if more vehicles are made, the total number of automotive displays shipped might stop growing. This shift challenges panel makers who previously relied on multi-display installations to drive shipment growth.

High-End Display Innovation and Premium Vehicle Penetration

As cockpit designs evolve to support more immersive, responsive, and visually appealing user experiences, the market is opening opportunities for innovation in high-performance display technologies. These include OLED displays, flexible panels, augmented reality (AR) HUDs, and panoramic curved screens that wrap across the dashboard. Additionally, the development of displays with integrated driver monitoring, haptic feedback, and gesture control is offering differentiation for automakers and Tier-1 suppliers. This innovation wave is expected to be led by premium vehicle segments, where consumers demand cutting-edge infotainment and safety systems.

Localization Strategies and Supplier Ecosystem Expansion

In response to trade tensions and supply chain constraints, OEMs are increasingly localizing their display production and sourcing strategies. This opens market opportunities for regional suppliers, particularly in India, Eastern Europe, and Southeast Asia, to enter the automotive display value chain. Strategic partnerships, technology licensing, and vertical integration with semiconductor and software providers will further enable manufacturers to capitalize on regional demand while mitigating global risks.

|

Attributes |

Details |

|

Market Value in 2024 |

USD 19.72 Billion |

|

CAGR % 2025-2034 |

7.46% |

|

Forecast Value in 2034 |

USD 40.23 Billion |

|

Base/Assessment Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

|

|

Report Coverage |

Market sizing, estimation & forecasting, market share analysis, YoY growth analysis, market dynamics and trends, regulatory landscape, strategic insights, and market opportunity assessment. |

|

Segments Covered |

Product Type, Screen Size, Display Technology, Vehicle Type, Application, Vehicle Class, and Distribution Channel. |

|

Regional Scope |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

|

Countries Scope |

U.S., Canada, Brazil, Argentina, Mexico, U.K., Germany, France, Italy, Spain, Russia, China, India, Japan, South Korea, Australia, UAE, Saudi Arabia, UAE, South Africa, and Rest of World* |

|

Key Companies Profiles |

Alpine Electronics, Inc., BOE Technology Group Co., Ltd., Continental Automotive, Denso Corporation, Harman International, Hyundai Mobis Co., Ltd., Japan Display Inc., LG Display Co., Ltd., Marelli Holdings Co., Ltd., Nippon Seiki Co. Ltd, Panasonic Corporation, Robert Bosch GmbH, Samsung Display Co., Ltd., Valeo SA, Visteon Corporation, and Yazaki Corporation. |

|

Customization Available |

Yes, the report can be customized to meet your specific requirements. |

MARKET INSIGHTS: BY PRODUCT TYPE

Based on product type, the market is segmented into Center Stack Display, Instrument Cluster Display, Head-Up Display, Rear-Seat Entertainment Display, and Smart Mirror Replacement Display. Among these, the Center Stack Display segment held the largest market share of around 38.5% in 2024. This dominance is attributed to its central role in infotainment and vehicle control systems, providing users with access to navigation, multimedia, and climate control. The growing integration of touchscreen interfaces and smartphone connectivity has further solidified its importance across mid-range and high-end vehicles.

MARKET INSIGHTS: BY SCREEN SIZE

Based on screen size, the market is categorized into Less than 6”, 6” to 10”, and Above 10”. In 2024, the 6” to 10” category accounted for the highest market share, owing to its widespread adoption across passenger vehicles for infotainment and cluster display applications. However, the Above 10” segment is witnessing rapid growth, driven by consumer demand for immersive in-car experiences and the trend toward panoramic and curved screen installations in premium models.

MARKET INSIGHTS: BY DISPLAY TECHNOLOGY

The market by display technology includes TFT-LCD, OLED (Passive Matrix OLED and Active Matrix OLED), Micro-LED, and Others. TFT-LCD remained the most widely used technology in 2024 due to its cost-effectiveness, durability, and adaptability across various screen sizes. However, OLED displays—especially Active Matrix OLEDs—are rapidly gaining momentum in luxury vehicles for their superior contrast, vibrant colors, and thinner form factor. Emerging Micro-LED technology is also gaining interest for its brightness and longevity, particularly in high-end and future concept vehicles.

MARKET INSIGHTS: BY VEHICLE TYPE

Based on vehicle type, the market is divided into Passenger Vehicles and Commercial Vehicles. The Passenger Vehicle segment led the market in 2024 with more than 80% market share, supported by rising adoption of digital cockpits, infotainment systems, and ADAS displays. As automakers increasingly differentiate vehicles through interior technology, the role of displays in passenger comfort and engagement continues to expand.

MARKET INSIGHTS: BY APPLICATION

Based on application, the market is segmented into Navigation, Multimedia / Infotainment, Telematics, Driver Assistance Systems, and Others. Among these, Multimedia / Infotainment was the leading segment in 2024. Increasing consumer expectations for connected and interactive experiences are fueling the demand for display-driven entertainment and control systems. Meanwhile, Driver Assistance Systems applications are also witnessing strong growth due to regulatory focus on safety and real-time driver information.

MARKET INSIGHTS: BY VEHICLE CLASS

By vehicle class, the market is categorized into Economy, Mid-segment, and Luxury. The Mid-segment class held the largest share in 2024, driven by growing availability of advanced display features in affordable models, especially in Asia-Pacific and Latin America. Meanwhile, the Luxury segment continues to push innovation, integrating multiple high-resolution displays, 3D visualization, and AI-based interfaces to enhance the in-cabin experience.

MARKET INSIGHTS: BY DISTRIBUTION CHANNEL

Based on distribution channel, the market is segmented into OEM and Aftermarket. OEMs captured the largest share in 2024, as displays are now standard or optional features in nearly all new vehicles. Automakers are heavily investing in proprietary infotainment ecosystems and digital instrument panels. However, the Aftermarket is showing steady growth, particularly in developing markets, where consumers seek to upgrade older vehicles with modern display systems.

Based on geography, the global automotive display market is segmented into North America, Latin America, Europe, Asia-Pacific, and the Middle East & Africa. Asia-Pacific leads the market, accounting for approximately 43.5% of the total share in 2024. This dominance is fueled by the region's high vehicle production, particularly in China, Japan, South Korea, and India, along with growing consumer demand for in-car digital experiences.

China: The Global Leader in Volume and Supply Chain Dominance

China remains the largest automotive display market by volume, supported by the government's aggressive promotion of New Energy Vehicles (NEVs) and policies that encourage domestic sourcing of electronic components. In 2024, Chinese panel manufacturers surpassed a 50% share of the global automotive display market. The country’s dominance is driven by strong local demand, a rapidly expanding EV industry, and support for vertically integrated supply chains. Global automakers operating in China have adapted by integrating localized display technologies into vehicle platforms to remain competitive.

United States, Germany, Japan: Premium Market Innovation Hubs

In markets such as the U.S., Germany, and Japan, the shift toward fully digital cockpits and large-format infotainment panels is well underway. These regions are home to several leading OEMs and Tier-1 suppliers that are investing heavily in display integration, AR HUDs, and curved OLED technologies. Regulatory emphasis on driver assistance, safety, and distraction reduction is also accelerating the adoption of intelligent display systems. The ongoing transition to Level 2+ and Level 3 autonomous vehicles is expected to further boost the demand for advanced in-cabin visualization systems.

Asia-Pacific (Exec. China): Growth Engine for Mid-Tier Display Adoption

Countries such as India, South Korea, Thailand, and Vietnam are seeing rapid growth in mid-range vehicle production with increasing integration of digital instrument clusters and infotainment displays. Falling component costs and rising consumer expectations for digital interfaces are fueling this trend. Regional governments are also incentivizing domestic electronics manufacturing, which could help position Asia-Pacific as a future hub for automotive display exports.

Latin America and Middle East: Emerging Demand with Infrastructure Constraints

In Latin America and parts of the Middle East & Africa, the market remains in early stages of digital cockpit penetration. While the premium segment is adopting advanced display features, mass-market adoption is constrained by limited EV infrastructure, high import dependency, and vehicle affordability issues. However, as urbanization and digital infrastructure improve, these regions are expected to present long-term growth potential, particularly for cost-optimized display solutions.

The global automotive display market features a highly competitive and vertically integrated landscape, with Tier-1 and Tier-2 suppliers playing distinct but interdependent roles across the value chain. Tier-1 suppliers—those directly partnering with OEMs to deliver fully integrated infotainment and instrument cluster systems—include leading players such as Bosch, Continental Automotive, Denso, Panasonic, LG Vehicle Solution, Visteon, Alpine, Hyundai Mobis, and Nippon Seiki. These companies are responsible for system design, software integration, HMI development, and in some cases, complete cockpit modules, aligning their solutions with OEM requirements for safety, design, and user experience.

Supporting these system integrators are Tier-2 suppliers, primarily responsible for providing the core display panels used in automotive applications. This group includes major display manufacturers such as LG Display, Samsung Display, BOE, AU Optronics, Japan Display Inc., Innolux, Tianma Microelectronics, ChinaStar, Truly, Giantplus, Sharp Display, and HKC Display. These companies supply high-resolution TFT, OLED, and Mini-LED panels that form the visual core of infotainment screens, digital instrument clusters, and head-up displays. With innovations in curved and ultra-wide screens, as well as cost-effective display manufacturing, Tier-2 players remain critical to scaling advanced display adoption across both premium and mid-market vehicle segments. The ongoing push toward fully digital cockpits and increased localization of supply chains—particularly in Asia-Pacific—is further intensifying competition among both tiers.

|

Segments |

Categories |

|

By Product Type |

|

|

By Screen Size |

|

|

By Display Technology |

|

|

By Vehicle Type |

|

|

By Application |

|

|

By Vehicle Class |

|

|

By Distribution Channel |

|

1 Methodology and Scope

1.1 Market segmentation & scope

1.2 Information Procurement

1.2.1 Purchased Database

1.2.2 Eternity’s Internal Database

1.2.3 Secondary sources & third-party perspectives

1.2.4 Primary Research

1.3 Information analysis

1.4 Market formulation & data visualization

1.5 Data validation & publishing

2 Executive Summary

3 Automotive Display Market Variables, Trends & Scope

3.1 Market Dynamics

3.1.1 Market Driver Analysis

3.1.2 Market Restraints

3.1.3 Market Challenge Analysis

3.1.4 Market Opportunities

3.1.5 Micro & Macro Indicator

3.2 Impact of COVID-19 Pandemic on Global Automotive Display Market

3.2.1 Overview of Changing Landscape

3.2.2 Pre-covid & Post-Covid Market Analysis

3.3 Market Attractiveness Analysis

3.4 Regulatory Scenario

3.5 Industry Trend Analysis- Historic and Future Trend Assessment

3.6 Merger & Acquisition

3.7 New System Launch/Approvals

3.8 Market Analysis Tools

3.8.1 Porter’s Five Forces

3.8.2 PEST Analysis

3.8.3 Value Chain Analysis

3.9 Key Company Ranking Analysis, 2020

4 Global Automotive Display Market Analysis and Forecast, By Type

4.1 Overview & Definition

4.2 Key Trends

4.3 Global Automotive Display Market Value (US$ Mn) Forecast, by Type (2019 – 2028)

4.2.1 Type 1

4.2.2 Type 2

4.2.3 Type 3

4.2.4 Type 4

4.2.5 Type 5

4.4 Type Comparison Matrix

4.5 Global Automotive Display Market Attractiveness, By Type

5 Global Automotive Display Market Analysis and Forecast, By Application

5.1 Overview & Definition

5.2 Key Trends

5.3 Global Automotive Display Market Value (US$ Mn) Forecast, by Application (2019 – 2028)

5.3.1 Application 1

5.3.2 Application 2

5.3.3 Application 3

5.3.4 Application 4

5.3.5 Application 5

5.4 Application Comparison Matrix

5.5 Global Automotive Display Market Attractiveness, by Application

6 Global Automotive Display Market Analysis and Forecast, By Region

6.1 Overview & Definition

6.2 Key Trends

6.3 Global Automotive Display Market Value (US$ Mn) Forecast, by Region (2019 – 2028)

6.4 North America

6.5 Europe

6.6 Asia Pacific

6.7 Latin America

6.8 Middle East & Africa

7 Global Automotive Display Market Attractiveness, by Region

8 North America Automotive Display Market Analysis and Forecast

8.1 Key Findings

8.2 North America Automotive Display Market Analysis (US$ Mn) and Forecast, By Type (2019-2028)

8.2.1 Type 1

8.2.2 Type 2

8.2.3 Type 3

8.2.4 Type 4

8.2.5 Type 5

8.3 North America Automotive Display Market Analysis (US$ Mn) and Forecast, By Application (2019-2028)

8.3.1 Application 1

8.3.2 Application 2

8.3.3 Application 3

8.3.4 Application 4

8.3.5 Application 5

8.4 North America Automotive Display Market Analysis (US$ Mn) and Forecast, By Country (2019-2028)

8.4.1 U.S.

8.4.2 Canada

8.4.3 Rest of North America

8.5 North America Automotive Display Market Attractiveness Analysis

8.5.1 By Type

8.5.2 By Application

8.5.3 By Country

9 Europe Automotive Display Market Analysis and Forecast

9.1 Key Findings

9.2 Europe Automotive Display Market Analysis (US$ Mn) and Forecast, By Type (2019-2028)

9.2.1 Type 1

9.2.2 Type 2

9.2.3 Type 3

9.2.4 Type 4

9.2.5 Type 5

9.3 Europe Automotive Display Market Analysis (US$ Mn) and Forecast, By Application (2019-2028)

9.3.1 Application 1

9.3.2 Application 2

9.3.3 Application 3

9.3.4 Application 4

9.3.5 Application 5

9.4 Europe Automotive Display Market Analysis (US$ Mn) and Forecast, By Country (2019-2028)

9.4.1 U.K.

9.4.2 Germany

9.4.3 France

9.4.4 Italy

9.4.5 Rest of Europe

9.5 Europe Automotive Display Market Attractiveness Analysis

9.5.1 By Type

9.5.2 By Application

9.5.3 By Country

10 Asia Pacific Automotive Display Market Analysis and Forecast

10.1 Key Findings

10.2 Asia Pacific Automotive Display Market Analysis (US$ Mn) and Forecast, By Type (2019-2028)

10.2.1 Type 1

10.2.2 Type 2

10.2.3 Type 3

10.2.4 Type 4

10.2.5 Type 5

10.3 Asia Pacific Automotive Display Market Analysis (US$ Mn) and Forecast, By Application (2019-2028)

10.3.1 Application 1

10.3.2 Application 2

10.3.3 Application 3

10.3.4 Application 4

10.3.5 Application 5

10.4 Asia Pacific Automotive Display Market Analysis (US$ Mn) and Forecast, By Country (2019-2028)

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 South Korea

10.4.5 Rest of APAC

10.5 Asia Pacific Automotive Display Market Attractiveness Analysis

10.5.1 By Type

10.5.2 By Application

10.5.3 By Country

11 Latin America Automotive Display Market Analysis and Forecast

11.1 Key Findings

11.2 Latin America Automotive Display Market Analysis (US$ Mn) and Forecast, By Type (2019-2028)

11.2.1 Type 1

11.2.2 Type 2

11.2.3 Type 3

11.2.4 Type 4

11.2.5 Type 5

11.3 Latin America Automotive Display Market Analysis (US$ Mn) and Forecast, By Application (2019-2028)

11.3.1 Application 1

11.3.2 Application 2

11.3.3 Application 3

11.3.4 Application 4

11.3.5 Application 5

11.4 Latin America Automotive Display Market Analysis (US$ Mn) and Forecast, By Country (2019-2028)

11.4.1 Brazil

11.4.2 Rest of Latin America China

11.5 Latin America Automotive Display Market Attractiveness Analysis

11.5.1 By Type

11.5.2 By Application

11.5.3 By Country

12 Middle East & Africa (MEA) Automotive Display Market Analysis and Forecast

12.1 Key Findings

12.2 Middle East & Africa (MEA) Automotive Display Market Analysis (US$ Mn) and Forecast, By Product Type (2019-2028)

12.2.1 Type 1

12.2.2 Type 2

12.2.3 Type 3

12.2.4 Type 4

12.2.5 Type 5

12.3 Middle East & Africa (MEA) Automotive Display Market Analysis (US$ Mn) and Forecast, By Application (2019-2028)

12.3.1 Application 1

12.3.2 Application 2

12.3.3 Application 3

12.3.4 Application 4

12.3.5 Application 5

12.4 Middle East & Africa (MEA) Automotive Display Market Analysis (US$ Mn) and Forecast, By Country (2019-2028)

12.4.1 GCC Countries

12.4.2 South Africa

12.4.3 Rest of MEA

12.5 Middle East & Africa (MEA) Automotive Display Market Attractiveness Analysis

12.5.1 By Type

12.5.2 By Application

12.5.3 By Country

13 Competitive Landscape

13.1 Market Players – Competition Matrix

13.2 Market Share Analysis by Key Players, 2020 (%)

13.3 Company Profiles

13.3.1 Company 1

13.3.1.1 Company Overview

13.3.1.2 Company Snapshot

13.3.1.3 Financial Overview

13.3.1.4 Product Portfolio

13.3.1.5 Key Developments/Strategies

13.3.2 Company 2

13.3.3 Company 3

13.3.4 Company 4

13.3.5 Company 5

13.3.6 Company 6

13.3.7 Company 7

13.3.8 Company 8

13.3.9 Company 9

13.3.10 Company 10

14 Key Takeaways

To ensure high-level data integrity, accurate analysis, and impeccable forecasts

For complete satisfaction

On-demand customization of scope of the report to exactly meet your needs

Targeted market view to provide pertinent information and save time of readers

A faster and efficient way to cater to the needs with continuous iteration

Focus on Data Accuracy & Reliability

75+ Clients in Fortune 500

All your transactions are secured end-to-end, ensuring a satisfactory purchase

Ensure the best and affordable pricing

![]()